The Difference Between Being Cash Poor and Asset Poor, and Why It Matters

Most people assume that if you own things of value, you're fine financially. But owning a house, a stock portfolio, or a retirement account doesn't automatically mean you can pay your rent this month. Two people can both be struggling financially for completely opposite reasons, and the fix for each is totally different. Understanding the gap between being cash poor and being asset poor is one of the most underrated concepts in personal finance, and getting it wrong costs people real money.

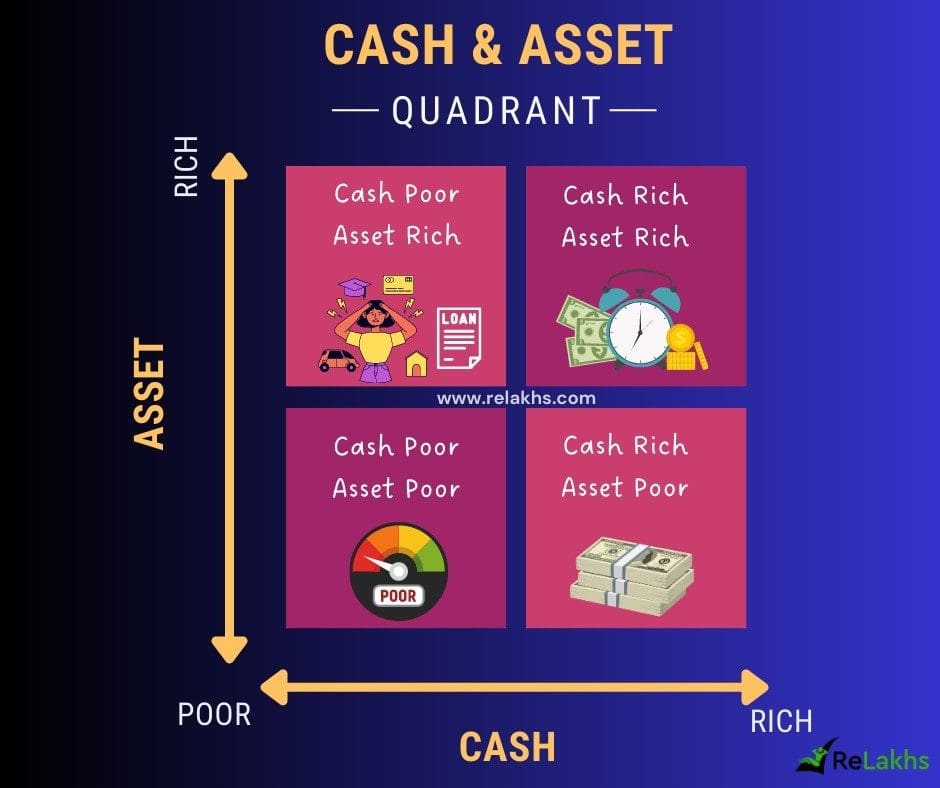

What It Actually Means: Cash Poor vs. Asset Poor

These two conditions sound similar but describe opposite financial problems.

Cash poor means you have limited liquid money available, even if you hold significant assets. Your net worth might look healthy on paper, but you can't easily access funds to cover everyday expenses, emergencies, or short-term obligations. You might be asset-rich, holding substantial real estate, business equity, or personal property, while still lacking the ready cash to cover day-to-day expenses.

Asset poor is the other side. You might have steady cash flow, a decent income, or money sitting in a checking account, but you've built little to no wealth in the form of assets that grow over time. No investments, no property, no equity. You're liquid, but not building anything.

Both situations create financial vulnerability. They just do it differently, and they require different strategies to fix.

How the Two Conditions Work in Practice

The confusion between cash poor and asset poor often comes from conflating net worth with financial health. They're related, but not the same thing.

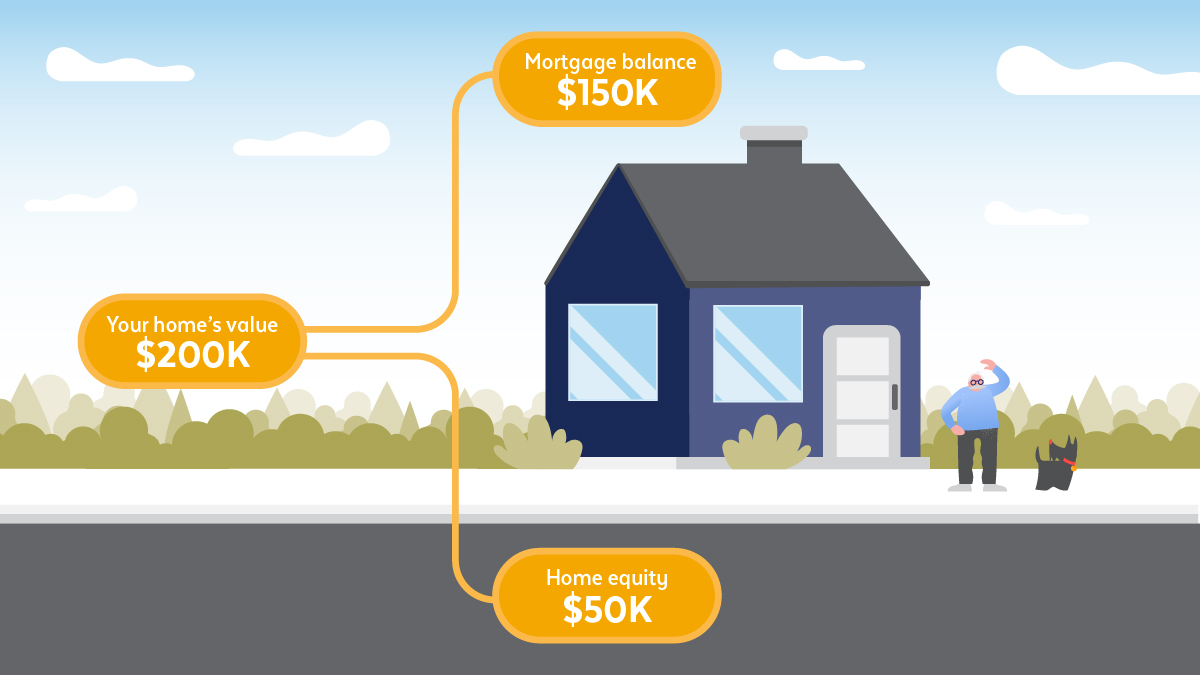

A homeowner who bought a house 20 years ago might have $400,000 in home equity but only $3,000 in their checking account. They're cash poor. If the roof needs replacing or they lose their job, that equity doesn't help them immediately. They'd need to sell, refinance, or take out a home equity loan to access it, with each option carrying its own cost and timeline.

On the other end, someone earning $80,000 a year who spends almost all of it on lifestyle expenses might have strong monthly cash flow but zero assets. No investments, no property, no ownership stake in anything that compounds over time. They're asset poor. A few bad months and they're in serious trouble with nothing to fall back on.

Cash is technically a subset of financial assets, but it's entirely possible to hold significant assets while remaining cash poor. Assets like real estate, business equity, or retirement accounts don't automatically convert to spendable money when you need it.

Why the Distinction Matters: The Real Financial Risk

Getting this wrong leads to predictable, avoidable mistakes.

People who are cash poor but asset rich often face a brutal choice: sell assets at the wrong time, or take on debt just to cover normal expenses. Selling assets to fund daily life is expensive in multiple ways. You lose the future compounding on whatever you sell. You may trigger capital gains tax. And you're often forced to sell at a time convenient for your bills, not optimal for the market.

People who are asset poor but cash rich face a different trap. They feel financially stable because money comes in regularly, but they're not building anything. Inflation erodes the purchasing power of cash sitting in low-yield accounts. Time passes. And the opportunity cost of not investing compounds against them every year.

The most dangerous position is being both, which is more common than most people admit. Low income, no savings, no investments, no equity. That's genuine financial fragility, and it leaves almost no margin for error.

Step-by-Step: How to Assess Your Own Position

1. List all your assets and categorize them by liquidity. Separate what you can access within 24 hours (cash, checking accounts) from what takes days or weeks (brokerage accounts, crypto) and what takes months or more (real estate, retirement accounts before age 59½, business equity).

2. Calculate your liquid coverage ratio. How many months of essential expenses can your liquid assets cover? Under one month is a red flag regardless of your total net worth.

3. Look at your asset-building rate. What percentage of your income is going into assets that grow? If the answer is close to zero, you may be cash-comfortable but asset poor.

4. Identify your actual bottleneck. Is your problem that you have assets but can't access them? Or that you have cash flow but nothing is compounding? The fix is different for each.

5. Map your cash flow against your asset growth. You want both. Enough liquidity to handle life without forced selling, and enough assets growing to build real wealth over time.

Common Examples and Mistakes

The Over-Invested Earner

Someone who puts every spare dollar into their 401(k) or a brokerage account but keeps almost nothing liquid. On paper, their wealth is growing. In practice, they're one emergency away from taking a 401(k) loan or selling investments at a loss. They're building assets, but they've created a cash poor problem in the process.

The High Earner Who Saves Nothing

A common pattern, especially when income grows alongside lifestyle. Strong cash flow, impressive salary, but no assets accumulating. The income feels like security, but it isn't. It stops the moment the job does. This is asset poverty hiding behind a decent paycheck.

The Retiree Trapped in Home Equity

A significant portion of American retirees hold most of their net worth in their primary residence. Overinvestment in illiquid assets like real estate can limit access to cash precisely when it's needed most. In retirement, that can mean being forced to sell the home or take on debt just to cover healthcare or living costs.

The Mistake of Treating Net Worth as Financial Health

Net worth is a snapshot. Financial health is about flow and flexibility. A high net worth with no liquidity and no income-generating assets is a fragile position. The goal is to build assets that both grow over time and can be accessed or borrowed against without triggering a forced sale.

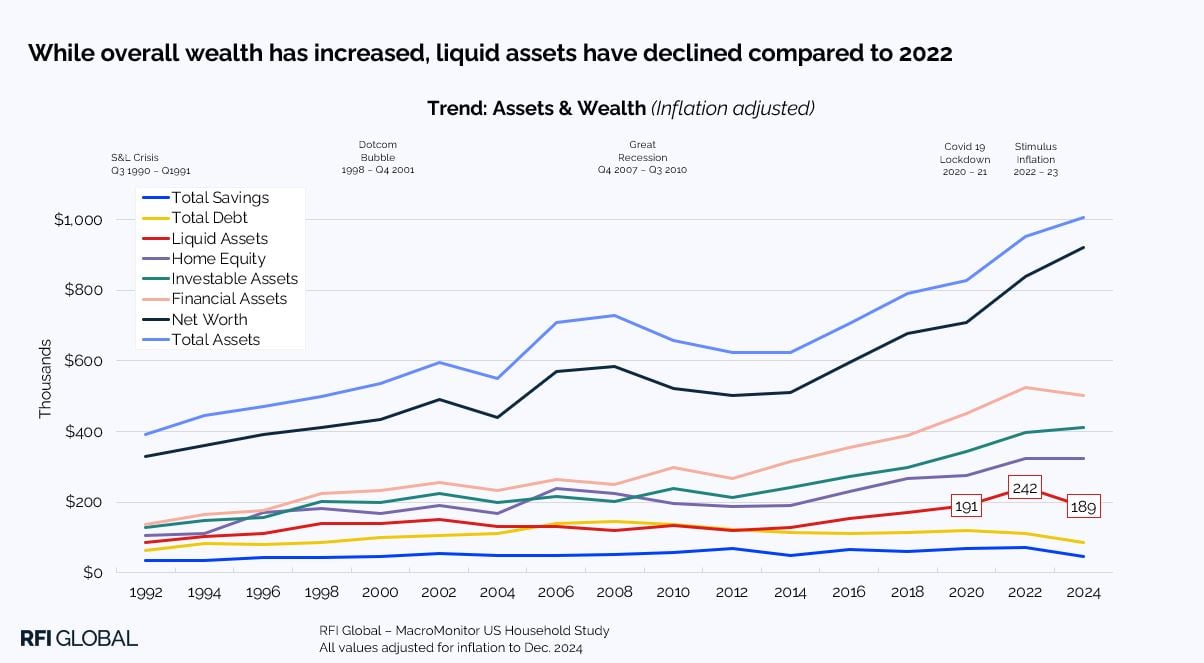

How This Connects to the Cost of Living Crisis

This distinction has become more urgent because of where the economy is right now. Wages have grown, but so has the cost of housing, healthcare, and basic goods. Many people are earning more than previous generations in nominal terms but building less wealth because more of their income goes to expenses before any of it reaches an investment account.

That dynamic creates a specific kind of asset poverty. People aren't broke in the traditional sense. They have income, they have spending power. But they're not accumulating assets that compound. And without compounding, income alone doesn't build wealth over time.

The smarter response to this pressure is restructuring how money flows before it gets spent. The traditional model works like this: earn, spend, save what's left. The problem is that "what's left" keeps shrinking. A different approach flips that sequence, getting assets working before expenses eat the income. That's where concepts like earning yield on assets you hold, borrowing against a portfolio instead of liquidating it, and keeping capital invested rather than idle start to make practical sense.

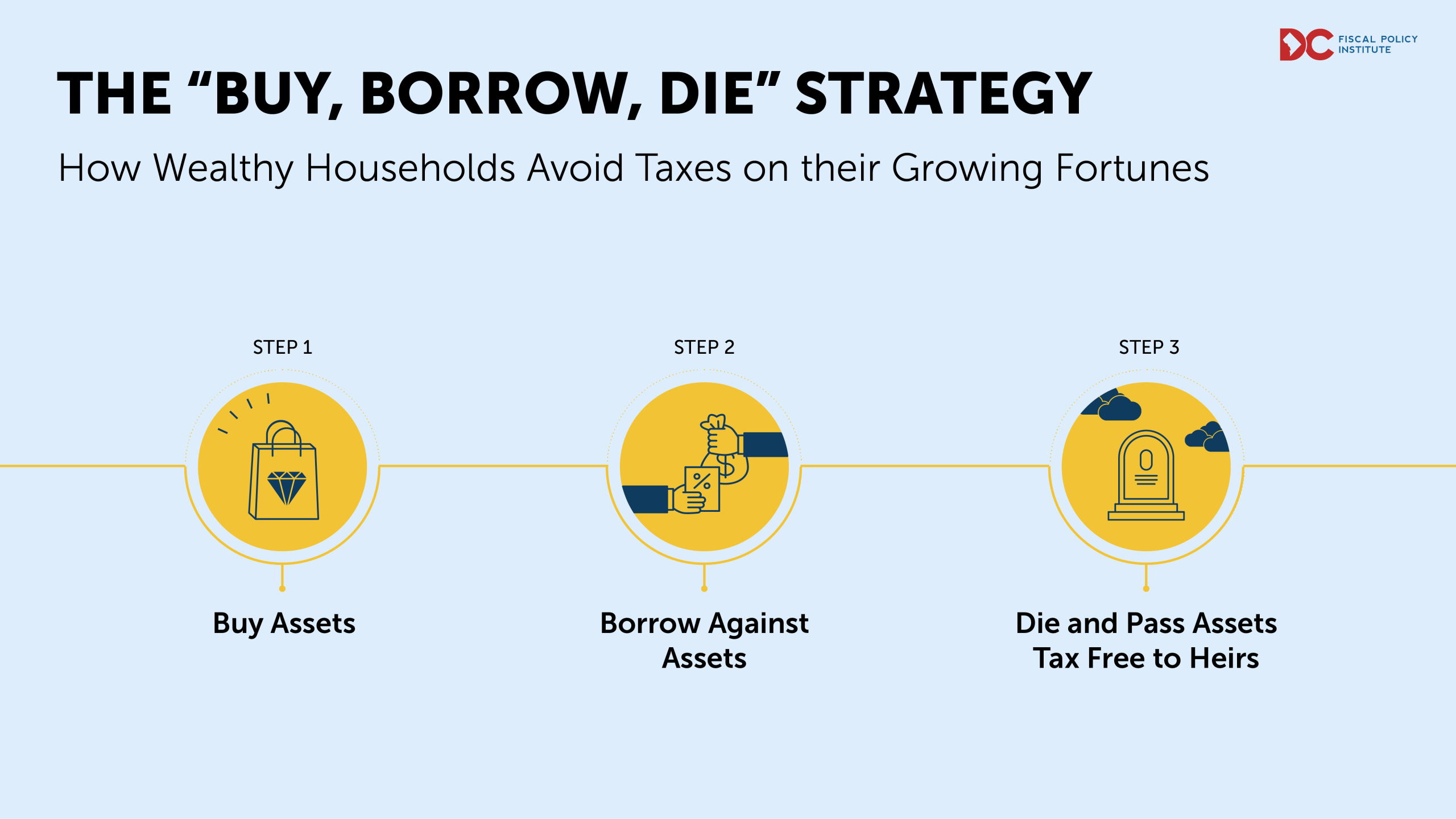

The "buy, borrow, die" strategy that wealthy families have used for decades is built on exactly this principle: never sell assets if you can borrow against them instead, avoid capital gains tax, and let compounding do the work.

The cost of living crisis hasn't made wealth-building impossible. It's made the old approach (save cash, spend cash, hope for the best) visibly inadequate. That's forcing a sharper conversation about what financial health really means and how to build it with the income you have, not the income you wish you had.

Frequently Asked Questions

What is the difference between being cash poor and asset poor?

Being cash poor means you hold significant assets but lack liquid money to cover everyday expenses or emergencies. Being asset poor means you have cash flow or liquid funds but haven't built assets that grow over time. Both create financial vulnerability, but they require different solutions.

Can you be both cash poor and asset poor at the same time?

Yes. Having low income, minimal savings, and no investments or equity puts you in both categories simultaneously. This is the most financially fragile position because there's no buffer from either direction.

What mistakes should people avoid when managing cash vs. assets?

Common mistakes include over-investing to the point of having no liquid reserves, treating high income as a substitute for asset accumulation, concentrating too much wealth in illiquid assets like real estate, and confusing net worth with financial flexibility.

How does the cost of living crisis relate to being cash poor or asset poor?

Rising costs consume more income before it can be invested, which drives asset poverty even among people with decent earnings. The traditional model of spending first and saving what's left produces weaker results when expenses keep growing. This is pushing more people to rethink how they structure their money flow.

How does earning more without building wealth connect to asset poverty?

Income and wealth are different things. Earning more raises your cash flow but doesn't automatically build assets. If higher income leads to higher spending without a proportional increase in investing, the result is asset poverty regardless of the salary number. Wealth comes from assets that compound, not from income that gets spent.

Is it better to be cash poor or asset poor?

Neither is a good position, but they carry different risks. Being cash poor with strong assets can create serious short-term problems including forced selling at bad times or taking on expensive debt. Being asset poor with cash flow feels stable but leaves you exposed over the long term as inflation erodes cash and nothing compounds. The goal is enough liquidity to handle life plus enough assets growing to build real wealth.

The content on this page is for informational purposes only and does not constitute financial, investment, legal, or tax advice.